Unlocking ERP’s Strategic Potential

Welcome to the second installment of our series exploring the intersection of enterprise resource planning (ERP) systems and effective management decision-making. In this segment, we embark on a journey to uncover the transformative potential of ERP solutions, illustrating how they can fundamentally reshape decision-making processes within organizations. By harnessing the power of information, companies can make informed decisions that enhance customer profitability, streamline operations, and improve service quality.

Yet, the path to successfully implementing and capitalizing on ERP initiatives is not without its challenges. It demands a well-defined strategy, significant resource investment, and unwavering leadership dedication. Many enterprises fail in their attempts to construct predictive models for business operations, overwhelmed by the complexities of the task. Consequently, they often resort to relying on historical financial metrics such as gross margin and net income, limiting the depth and accuracy of their decision-making to historical information.

Traditionally, the chief financial officer (CFO) is responsible for orchestrating this data-driven transformation, safeguarding the organization’s financial assets. As companies strive to construct their unique data-information-knowledge-wisdom (DIKW) triangle, it becomes imperative for business managers to leverage this wealth of information for both strategic and tactical decision-making. After all, the quality of insights gleaned from ERP systems directly influences organizational performance, especially in an ever-evolving business landscape shaped by technology, globalization, and regulatory and geopolitical events.

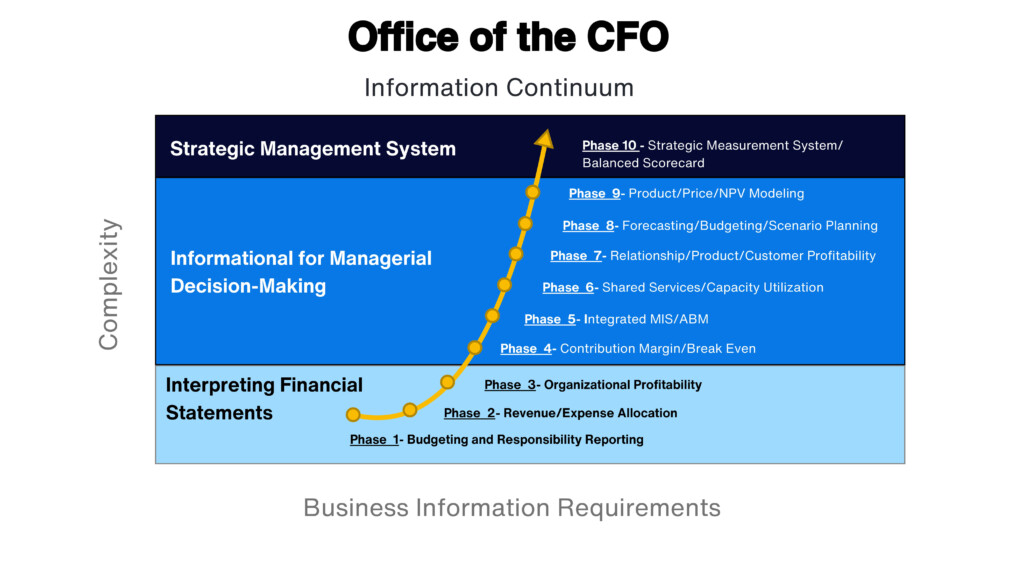

So, how does the DIKW framework, introduced in our previous discussion, intersect with ERP systems to enhance management decision-making? Through a systematic progression of a ten-key-step journey (see exhibit Office of the CFO), we explore how companies can transition from raw data to actionable information, unlocking the full potential of their informational assets. Ultimately, wisdom emerges as the culmination of knowledge joined with practical experience, underscoring the transformative impact of informed decision-making. Join us as we navigate this path together, unlocking new strategic insights and operational excellence.

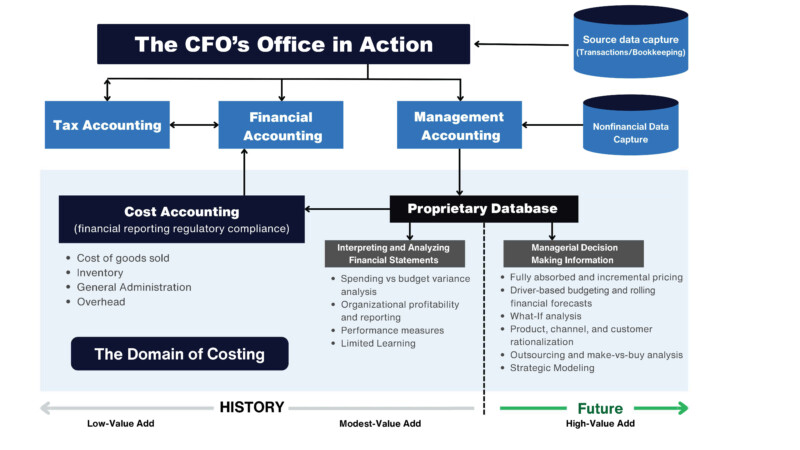

Interpreting and analyzing financial statements is a cornerstone of evaluating an organization’s financial well-being. It involves examining the balance sheet, income statement (see exhibit The CFO’s Office in Action), and cash flow statement to gauge performance, profitability, and liquidity. Key financial ratios such as return on equity, debt-to-equity, and current ratio offer valuable insights into efficiency and solvency. At the same time, trend analysis unveils patterns over time, aiding decision-making. Furthermore, benchmarking against industry standards provides competitive insights.

Phase 1: Budgeting and responsibility reporting

This phase of management’s financial journey revolves around budgeting and responsibility reporting. The focus depends on expense control and assigning accountability to individual managers. Management relies on budget reports, comparing actual expenses with budgeted costs and prior-year figures. Variance reports for executive scrutiny and revenue, profit, and growth goals shape this phase.

Phase 2: Revenue and expense allocation

Phase 2 shifts attention to revenue and expense allocations across the organization. This involves establishing mechanisms to allocate centralized or shared expenses, mostly fixed, often managed within the CFO’s office. These allocations, performed manually or through spreadsheets, align back-office expenses with revenue-generating units, enhancing overall profitability.

Phase 3: Organizational profitability

Phase 3 marks a strategic shift toward assessing organizational profitability at the business unit level. The aim is to establish accountability and measure performance accurately. Introducing transfer pricing methodologies and refining allocation methods are key strategies to enhance understanding of profitability and drive cost efficiencies. This phase emphasizes the allocation bases to foster a deeper understanding of overall profitability.

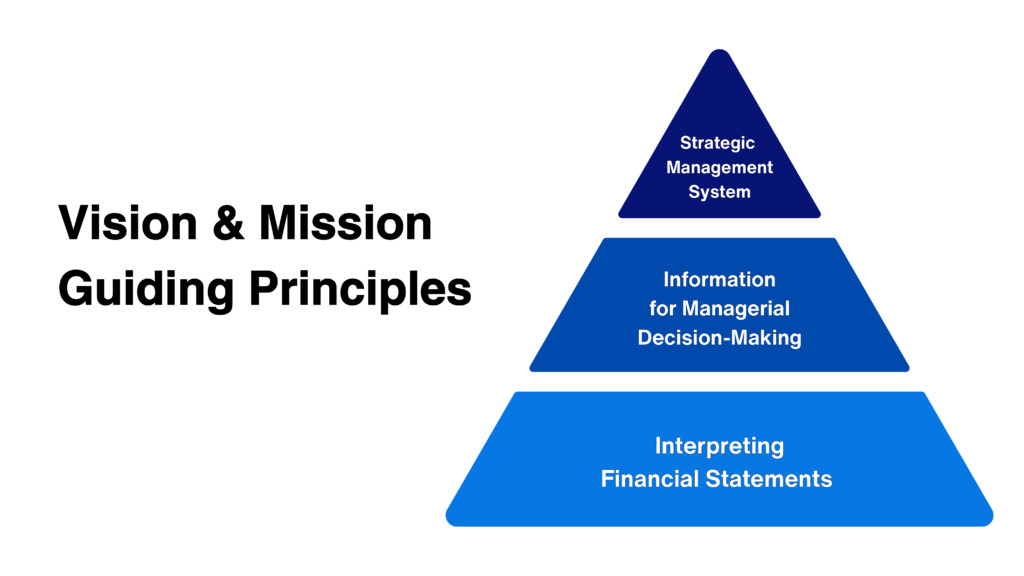

Managerial decision-making information progresses from interpreting and analyzing financial statements by incorporating non-financial data alongside financial insights. This evolution spans from contribution margin and integrated management information systems (MIS) to shared services, capacity utilization, and customer-product and/or service profitability, culminating in forecasting/rolling budgets/ operational and capital decision-making, along with product/pricing/net present value (NPV) modeling. These phases deepen our understanding of our customers and refine strategies for better service delivery (see exhibit Vision & Mission Guiding Principles).

Phase 4: Contribution margin/break even

Phase 4 starts to incorporate volume and non-financial metrics into decision-making. Contribution margin (CM), the surplus of sales revenue over variable costs, lies at the heart of cost-volume-profit (CVP) analysis. This tool forecasts the dynamics among revenues, variable costs, and fixed costs across production levels, facilitating insight into the effects of sales volume, pricing, costs, and product mix changes. In strategic planning, firms must consider several variables: product/service pricing, output levels to meet customer demand, projected costs, and resulting profit margins.

After selecting an implementation plan, a detailed budgeting process calculates the resources required and forecasts the plan’s financial impact. Preliminary analysis often relies on a simple tool grounded in the algebraic relationships among sales price, volume, unit variable cost, and total fixed cost.

Understanding the differing behaviors of variable and fixed costs in response to production volume changes is crucial for effective cost management. Fixed costs, driven by strategic decisions, ensure productive capacity alignment with customer needs, while variable costs fluctuate with short-term activity levels, such as weekly or monthly operational dynamics.

Phase 5: Integrated MIS/ABM

An integrated management information system (MIS) is the foundation of the organization’s ERP system. It resembles a structured database, housing financial and non-financial data on relationships, customers, products and services, and delivery channels. The integration of this system yields numerous benefits, including data consistency, streamlined processing efficiency, audit trails, and enhanced control over information dissemination. This integrated approach offers a multifaceted perspective on the contributions of products, customers, and organizational segments to overall profitability, allowing for insightful analysis down to the actual activity drivers.

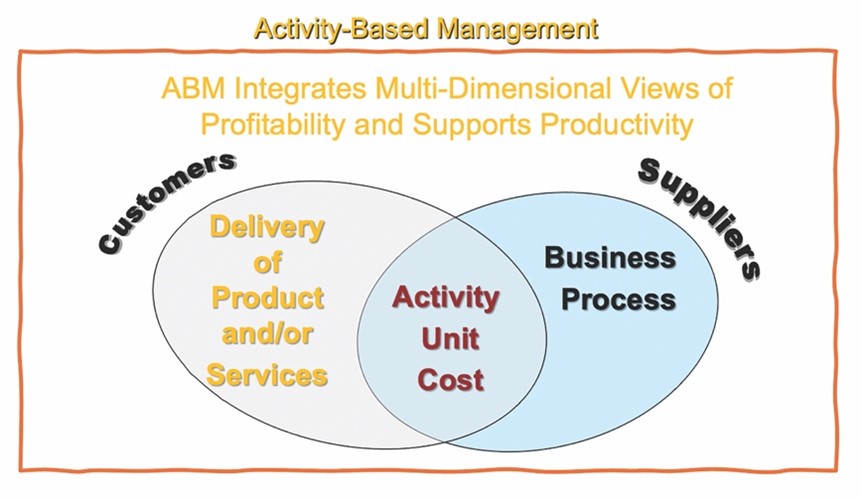

Central to this phase is the implementation of activity-based management (ABM), which manages and processes both financial and non-financial data, tracking the organization’s resources and consumption by customers and products. Moreover, companies leveraging shared services for planning, budgeting, and forecasting exhibit superior performance, with high-performing finance organizations completing forecasting cycles significantly faster than their competition (see exhibit ABM).

However, implementing an integrated performance measurement system and ABIS requires substantial resource investment. Components such as activity-based costing (ABC), activity-based analysis (ABA), activity-based budgeting (ABB), and activity-based pricing (ABP) are integral to this phase, offering advanced methodologies for profitability and productivity measurement/management, performance analysis, budget setting, and pricing strategies. These tools enable businesses to transcend reliance on historical data, driving informed decision-making and enhancing overall operational efficiency.

Phase 6: Shared services/capacity utilization

The purpose of a shared service unit is to consolidate and centralize specific business functions or services within an organization to streamline operations, improve efficiency, and reduce costs. Instead of each department or business unit handling these functions independently, such as finance, human resources, IT, or procurement, a shared service unit consolidates these activities into a centralized location or team. This allows for standardized processes, economies of scale, and expertise pooling. Shared service units often provide services internally to different departments or business units within the organization, acting as a centralized hub for delivering essential services efficiently and effectively.

Cost calculations are typically based on practical capacity utilization levels. Practical capacity, less than theoretical maximum capacity, reflects real-world operating conditions. The cost of available unused capacity is quantified and identified for accurate financial analysis.

Phase 7: Relationship/product/service profitability

Relationship/product/service profitability marks a pivotal stage where advanced technologies furnish management with comprehensive insights into ongoing profitability. Unlike earlier phases, this stage ensures holistic coverage, automating the systematic production of data. The primary aim is to eliminate credibility issues tied to ad-hoc profitability assessments and integrate dependable, timely information into decision-making processes.

With Phase 7, substantial staffing and resource investment become imperative, highlighting the organization’s recognition of information as a valuable asset. Here, management delves into uncovering the “true” profitability of customer relationships, transcending single products or services. This broader perspective enables better decision-making, particularly in product positioning and cross-selling strategies.

Moreover, this phase offers superior flexibility in customer relationship categorization, enhancing reporting flexibility and aiding in targeted marketing efforts. However, it also introduces additional data requirements, often beyond the scope of existing information systems. By embracing Phase 7, organizations gain deeper insights into customer relationships, laying the groundwork for more informed strategic decisions and sustainable profitability.

Phase 8: Forecasting/rolling budgets/operational and capital

Forecasting/rolling budgets/operational and capital marks a critical juncture where forecasting becomes paramount for managers to anticipate and adapt to changing conditions. It’s a planning tool that leverages past and present data, alongside trend analysis, to navigate future uncertainties. With management’s expertise and judgment, assumptions are projected into forthcoming periods using moving averages or regression analysis to identify trends.

Sensitivity analysis assigns range values to uncertainties to mitigate errors in assumptions, ensuring a robust forecasting framework. Best practice organizations often develop multiple forecast scenarios to account for varying conditions. It’s crucial to differentiate forecasting from budgeting. While budgets aid in planning, communication, and performance evaluation, forecasting encompasses the entire value chain, serving as an effective decision-making model for your organization.

Modern financial planning models react dynamically to diverse assumptions, allowing for agile responses to sales, costs, and product mix changes. While headquarters set policies, business units are pivotal in implementing and monitoring key performance indicators (KPIs) to drive these policies forward.

Phase 9: Product/price/NPV modeling

Product/price/NPV modeling, management shifts focus from merely analyzing historical profitability to strategic planning and modeling of products, services, customers, and their optimal mix. The intersection of organizational, product/service, customer, and relationship profitability, both historically and projected, takes center stage.

Product and NPV modeling broaden the utility of performance data. While earlier phases aid tactical decisions like pricing and cost reduction, this phase empowers management to make more informed strategic choices, such as new product introductions or optimizing existing offerings.

In this phase, reliance on historical data alone becomes insufficient. Online access to pertinent information becomes crucial, potentially offering a sustainable competitive advantage.

Net present value (NPV) emerges as the preferred metric for customer acquisition decisions, offering insights into the organization’s lifetime value and overall benefit. However, for decisions concerning existing relationships, where historical periods hold less relevance, net income for current and future periods may suffice.

Strategic management systems (SMS) facilitate organizations in navigating strategic planning and execution efficiently, aligning mission, vision, and objectives with resources, and achieving a sustainable competitive advantage and long-term success. By combining strategy formulation, implementation, and evaluation, SMS ensures that strategies are thoroughly crafted, executed, and continuously evaluated.

Phase 10: Strategic measurement system (SMS)/balanced scorecard

Phase 10 introduces the strategic measurement system (SMS) and the balanced scorecard, building upon earlier phases by acknowledging profitability as just one facet of success. These systems elevate non-financial metrics to equal importance with financial ones.

For instance, internal measures may include quality considerations, while customer measures cater to individual needs. Rather than replacing existing metrics, these systems complement lagging indicators with leading ones, facilitating proactive decision-making.

SMS and the balanced scorecard pinpoint value creation, highlight improvement opportunities, and gauge progress toward strategic objectives. They offer an integrated approach, emphasizing the most critical variables across activities, products, and processes. It’s vital that these measures align with the organization’s strategy, triggering management responses that support objectives. Careful selection ensures actionable measures that harmonize with each other, fostering coherent progress toward organizational goals.

Navigating the landscape of digital transformation in facility management requires adopting an ERP system and a strategic approach to utilizing the wealth of information it provides. As we steer our organizations through this evolution, the data we gather and analyze will serve as our guiding light, illuminating the path toward informed decision-making and sustainable growth.

ERP and management decision-making can help solve some of the significant problems our organizations face. Famous management consultant Peter Drucker once said, “What are the major problems faced by most organizations? Fundamentally, the confusion between effectiveness and efficiency stands between doing the right things and doing things right. There is surely nothing quite so useless as doing with great efficiency what should not be done at all.”

How much is your organization doing that should not be done at all?

In conclusion, ERP systems are pivotal in enhancing management decision-making processes by providing real-time insights, streamlining operations, and fostering collaboration across departments. However, the true power of these systems doesn’t just reside in their technological capabilities but in how effectively organizations integrate them into their broader strategy and culture.

Looking ahead, the final installment in this three-part series will discuss the principles of systems thinking and the importance of fostering a shared vision within the organization. By understanding the connectivity of various components within your business and aligning individual goals with overarching objectives, companies can cultivate a culture of innovation, adaptability, and resilience in the face of digital disruption.

Jon Hill is the CEO of Cobotiq and provides business managers with information on how to create and implement profitability. He is a frequent speaker and presenter on the future impact of automation and technology in the cleaning industry.

{kind=link}